Economic Update May 2024

The highlights:

Ongoing economic strength and unrelenting inflationary pressures in the United States (US) continued to dominate discussions in April. United States (US) consumer price index (CPI) data for March revealed a third successive month of higher-than-expected inflation, dashing hopes for early and aggressive rate cuts.

After an impressive performance by markets in the first quarter of 2024, the second quarter began on a weaker note. Concerns the US Federal Reserve (Fed) will keep interest rates higher for longer weighed on returns from shares and fixed interest (bonds).

After five straight months of gains, international shares retreated in April. The US market led the falls, with Australia following its global peers lower. However, Chinese shares bucked the trend, rebounding on optimism that the world’s second-largest economy is beginning to stabilise.

Returns from fixed interest markets were also negative, as bond yields pushed higher and bond prices moved lower. Credit (corporate bonds) performed better than long-duration government bonds.

Market observations

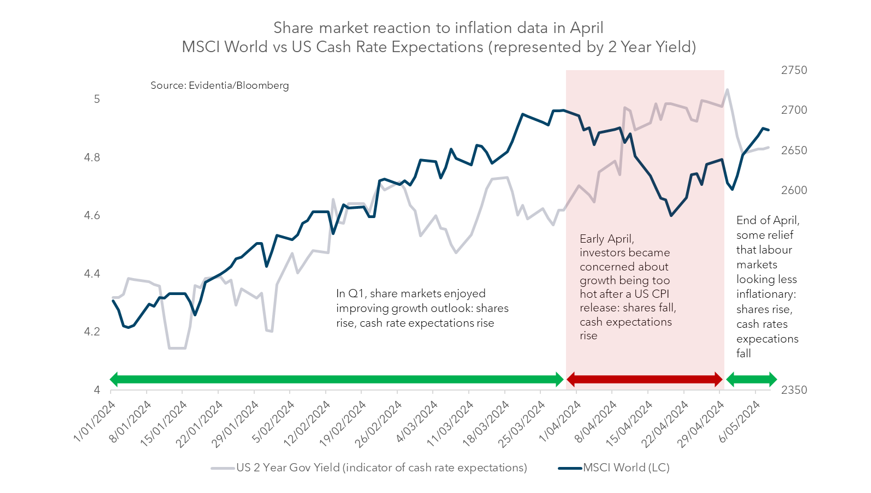

Strong global economic data throughout the first quarter of 2024 led to a continuation in the share market rally, as investors focused on the positives of an improving growth outlook. However, at the same time as shares were moving higher, the increasingly apparent strength of the US economy led investors to reduce the number of cash rate cuts expected from the Fed. The two-year US Treasury yield (an indicator of future expected cash rates) moved from 4.25% to 4.71% over the first quarter. Yet share markets seemed momentarily unphased by the rising yield curve and continued to bid up valuations.

The central theme in April was a shift in sentiment back to concerns about how sticky inflation may be and how long cash rates will remain at current levels. Share markets were sold off as a result.

This shift in sentiment accelerated on 11 April when a stronger-than-expected CP) print was released. While US headline CPI mildly overshot forecasts, within the data there was a broad ratchet up in almost all consumer price categories. This triggered a more anxious response from the market that inflation was not moderating at the pace hoped for. Annual US inflation is now 3.5%, which has been trending sideways for several months.

Globally, this fear spread, and even in Australia, where recent inflation results have been more encouraging, bond yields rose, and shares fell. A signature trait of a market sell-off — spurred by inflation and bond yield concerns — was that listed property, listed infrastructure, global small-caps, and growth sectors led the pull-back.

April reminded us of how hinged share markets are to inflation and bond yield outcomes at present. In our strategy, we focus on long-term views and mostly ignore near-term noise. We believe cash rates will stay where they are for some time in the US and Australia but eventually trend downwards. It is a question of when, not if, cash rates will fall. This, combined with a resilient global growth outlook, remains supportive of shares.

As the macro environment continues to improve, valuations are our main concern and keep us from moving overweight growth assets. We are also mindful of the outside risk that inflation persists to the degree that rates need to go higher. A backward pivot — where expectations of rate cuts shift to expectations of further rate hikes — would be damaging for markets.

Economic Review

Australia

Recent data indicated inflation continues to moderate in Australia but is declining more slowly than expected. The annual pace of headline CPI fell from 4.1% in the December quarter to 3.6% in the March quarter, which was below estimates of 3.5%. Annual core CPI — which excludes volatile items — slowed from 4.2% to 4.0%, but this was also higher than estimates.

As expected, the Reserve Bank of Australia (RBA) held rates at 4.35% at its early May meeting. However, in response to the stickier-than-expected inflation data, the RBA raised its cash rate forecast for December to 4.4%, up from the 3.9% it forecast three months ago. The RBA maintained it still expects core CPI to fall within its 2-3% target range in the second half of 2025.

Australia’s labour market remained relatively tight in March, with only a small drop in the number of jobs lost and a lift in the unemployment rate from 3.7% to 3.8% falling short of expectations.

US

Recent headline and core CPI rose quicker than expected, taking annual headline CPI from 3.2% in February to 3.5% in March. Core inflation remained flat at 3.8%. Released later in the month, core personal consumption expenditure (PCE) inflation — the Fed’s preferred measure — also ticked higher to 2.8%. The Fed’s target for core PCE is 2%.

Signs of a softening labour market provided investors with some reassurance the uptick in inflation may be temporary. The US economy added 175,000 jobs in April, falling short of market expectations. In its May meeting, the Fed maintained the federal funds rate at between 5.25% and 5.5%, emphasising that it doesn’t plan to cut rates until it has greater confidence that inflation is slowing sustainably to target.

Europe

Annual European inflation is expected to remain stable at 2.4% in April, according to a flash estimate from Eurostat, the statistical office of the European Union. The unemployment rate was also unchanged at 6.5% in March, down from 6.6% a year earlier.

The European Central Bank (ECB) is expected to announce a rate cut at its June meeting, although there are pockets of concern about stubborn services inflation and a delay by the Fed in easing monetary policy in the US could cause the bank to also postpone action.

Asia

A weakening yen — which dropped to 30-year lows before rebounding in late April — and core inflation falling beneath 3% for the first time since November 2022 to 2.9%, provided a complex backdrop for the Bank of Japan’s (BoJ’s) April policy meeting. In response, the BoJ left rates on hold at between 0% and 0.1%, maintaining its view the economy will sustainably achieve its 2% inflation target rate over the next two years despite concerns that weakness in the yen could trigger further inflationary pressures.

Asset Class Review

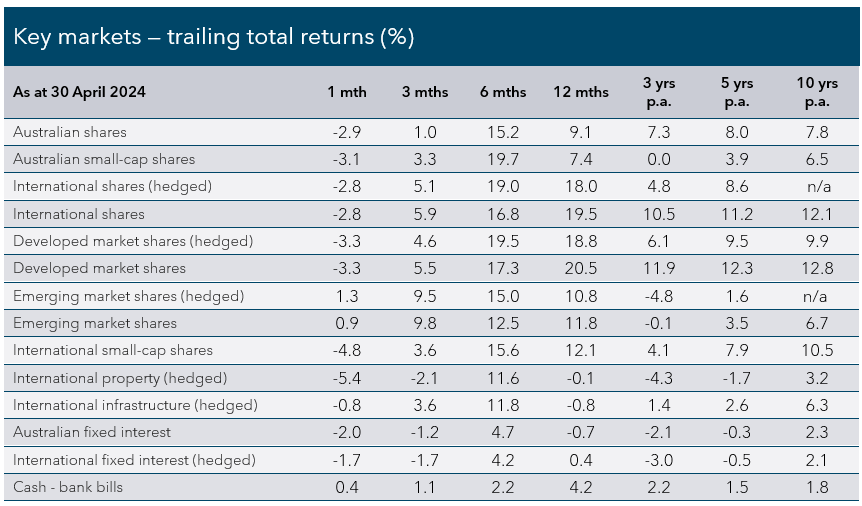

Australian Shares

Delays to the timeline for potential interest rate cuts applied downward pressure to shares in April, as investors locked in recent gains and moved to the sidelines. The S&P/ASX 200 Index fell -2.9% for the month, in step with global markets as a five-month-long rally petered out. The recent dominance of small companies over large reversed, as the S&P/ASX Small Ordinaries Index — more sensitive to interest rates — fell -3.1% in April.

All sectors dipped into negative territory in April with the exception of utilities (+4.8%) and materials (+0.6%). The former led the way thanks to investor demand for the sector’s defensive characteristics, along with a strong month for sector heavyweight Origin Energy which benefited from a lift in the oil price. Materials advanced thanks to a late-April uplift in commodity prices. Interest rate-sensitive sectors, which have led the recent rally, were the hardest hit. Real estate (-7.7%) was the worst-performing sector, reversing much of its recent gains on uncertainty about the timing of future interest rate cuts. Information technology (-3.9%) and consumer discretionary (-5.1%) sectors also retreated.

What fund managers are saying…

“While we believe that economic growth will continue to slow, for at least the first half of 2024, in Australia and in large parts of the world, we don’t think that Australia will move into a recession. Unemployment continues to be low, and the resumption of strong immigration and population growth will likely underpin the economy. Sectors like insurance, building and construction, communications, healthcare, diversified financials, and some consumer staples should remain strong or improve through 2024.

Over the longer term, Australia has been one of the best-performing equity markets in the world — driven by structural growth issues like population growth, corporate governance, a large and low-cost natural resource base, high dividend yield (driven by franking credits) and high real dividend growth (helped by capital discipline). These long-term structural drivers are still very much in place and should reassert themselves in 2024 as conditions continue to stabilise. This should bode well for Australia’s equities market – with over 2,000 listed companies, the domestic market is the world’s ninth largest and has consistently been among its best performers.“

Fidelity International

International Shares

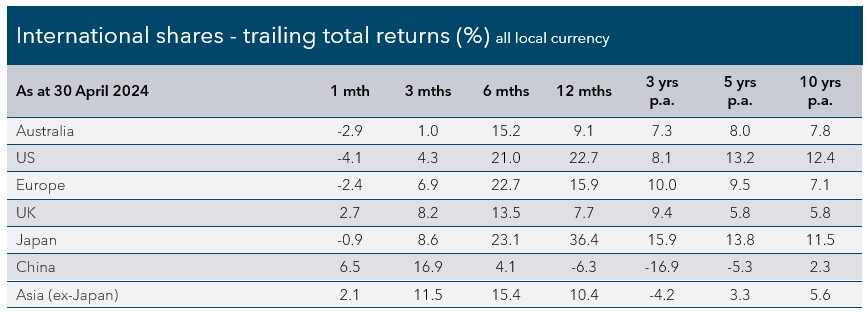

International shares fell in April amid concerns resurgent US inflation would push the start date of the Fed’s anticipated rate-cutting cycle further into the future. The MSCI All Country World Index dropped -2.8%, while a flat Australian dollar meant the hedged equivalent index fell by the same amount. Small companies ended the month well behind their larger peers, with the MSCI World ex Australia Small Cap Net Return AUD retreating -4.8%. Interest rate-sensitive sectors fared worst, with real estate (-6.8%), information technology (-5.5%) and consumer discretionary (-4.3%) all underperforming. Utilities (+1.2%) and energy (+0.8%) were bright spots for the month.

US shares reversed strong first-quarter gains, with the S&P 500 Index falling -4.1% and the tech-heavy Nasdaq Composite Index down -4.4%. The Euro Stoxx 50 Index — which tracks the performance of the European region’s 50 most influential companies — was -2.4% lower in April. The United Kingdom’s (UK) FTSE 100 Index was one major market that bucked the downward trend in April, rising +2.7% as a pick-up in economic growth, a weaker pound, and rising commodity prices benefited its high weighting to financial and resources sectors. The recent rally in Japanese shares lost momentum as the Topix Total Return Index gave up -0.9%. The MSCI Emerging Markets Index (Hedged) posted positive returns of +1.3% over the month. The gains in emerging markets were boosted by a strong rebound in Chinese shares that came off the back of a strong first-quarter GDP result which provided evidence that government support is beginning to gain traction — the MSCI China Net Total Return Index climbed +6.5%.

What fund managers are saying…

“The trajectory for stock markets ultimately hinges on the outlook for inflation, interest rates, and accordingly, the so-called ‘landing’ for the economy. Our high probability scenario is calling for a goldilocks “soft landing” scenario where inflation decelerates towards the 2% target without a meaningful deterioration in economic activity. This allows central banks to cut interest rates at early signs of economic weakness, keeping the economy not-too-hot or not-too-cold, but just right. An environment of disinflationary growth is unambiguously positive for stocks. In our main scenario, global equities would require both earnings growth (the ‘E’ in P/E) and central bank rate cuts (the ‘P’ in P/E) to validate current valuations and the potential for further upside. We assign a 50% probability to this optimistic scenario.

That being said, there are some notable risks to the outlook and recent stock market gains would undoubtedly be vulnerable should investors move to price-in an alternative scenario that includes either a restrained liquidity backdrop (‘Inflation Revival’ = 30%) and/or a deteriorating growth and earnings backdrop (‘Shallow Recession’ = 20%). On the former, the risk of a second wave of inflation would prompt a ‘hawkish’ policy response – namely the need for interest rates to remain higher for longer. In this scenario, upside surprises to both growth and inflation would prompt central banks to abandon plans to cut interest rates. Bond yields would revert higher in response and equity market valuations would contract. On the latter, economic growth deteriorates more meaningfully as the cumulative impact of past rate hikes begins to take its toll. While central banks would certainly step in and slash interest rates, it would not be soon enough to avert a mild recessionary outcome and a bear market in stocks..”

Fiera Capital

Property and Infrastructure

Rising bond yields triggered by expectations of higher-for-longer cash rates, weighed on the interest rate-sensitive global listed property sector, with the FTSE EPRA Nareit Developed Index (Hedged) falling -5.4%. Global listed infrastructure posted negative monthly returns but outpaced international shares by some margin, with investors attracted to the asset class's inflation-linked characteristics. The FTSE Global Core Infrastructure 50/50 (Hedged) Index retreated -0.8% in April.

Fixed Interest

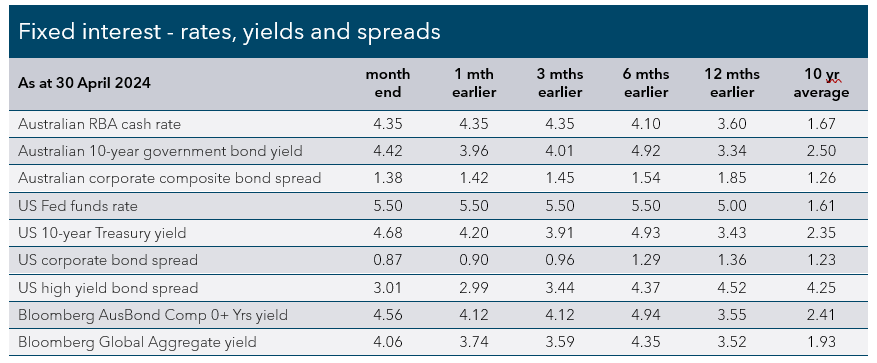

Resilient economic growth and hotter-than-expected inflation data in the US dashed hopes for early and aggressive rate cuts, pushing government bond yields higher and weighing on returns from fixed interest (bond) markets in April. Global and Australian bonds suffered equally from the change in rate expectations. The Bloomberg Global Aggregate Bond Hedged Index was down -1.7% in April, while the local Bloomberg AusBond Composite 0+ Yr Index retreated -2.0%. Both indices are heavily influenced by the performance of government bonds.

US Treasuries led the sell-off in global government bonds, with the 10-year US Treasury yield jumping 0.46% in April to 4.68% to its highest level since late 2023. Two-year US Treasury yields also spiked, rising 0.41% to 4.63%. The same dynamics were felt locally, with 10 and two-year Australian Government Bond yields jumping similar amounts to end April at 4.42% and 4.10%, respectively. Consequently, returns from government bonds were negative. The Bloomberg US Treasury Total Return Unhedged USD Index fell -2.3% and the Bloomberg AusBond Treasury 0+ Yr Index dropped -2.0% over the month.

Returns from credit markets (corporate bonds) were negative but performed well relative to government bonds, as spreads on high-quality investment-grade credit (the extra compensation a corporate bond must pay above the so-called risk-free rate offered on a government bond with a similar maturity date) tightened further, reflecting an improving economic outlook and reduction in potential default risk. Australian credit benchmark Bloomberg AusBond Credit 0+ Yr Index retreated -0.91% in April, while global credit — as measured by the Bloomberg Global Aggregate Credit Total Return Index Hedged AUD — fared worse, falling -1.92%. Global high yield credit again benefited in a relative sense from positive economic data, with losses from the Bloomberg Global High Yield Total Return Index Hedged AUD of -0.7% less severe.

What fund Managers are saying…

“The Australian economy is slowing gently, and while no recession is forecast, the pressure of higher interest rates is expected to continue to broaden out across sectors of the economy. Our base case is for the RBA to remain on hold at current rates before commencing an easing cycle late 2024. There is a myriad of risks to the base case at this stage, with the high case of no easing until 2025 and a slow cycle through to 2026, and the low case of a modestly earlier commencement. We see the near-term pricing hinting at a rate hike this year and very limited cuts in 2025, as underestimating the risks to the economy after a long period of policy tightness. We currently consider the Australian yield curve as under-valued at points in the curve. We hold a long duration position and look to add to it on any worsening of the economic outlook.

In recognition of the complex macroeconomic and geopolitical environment, our credit strategy remains skewed towards high-quality, investment grade issuers with resilient business models, solid earnings power and conservative balance sheets. While acknowledging that credit spreads in general have tightened considerably, all-in yields particularly in low/no default-risk investment grade credit remain highly attractive. We have been actively and selectively taking advantage of these yields in highly-rated corporate bonds and structured credit, particularly in the primary markets where transactions have come with new issue concessions.”

Janus Henderson

All financial services included in this communication are authorised by Infinity Financial Consultants, Infinity Financial Consultants Pty Ltd is a Corporate Authorised Representative of Infinity Advisor Australia Pty Ltd ABN 53 636 060 609 AFSL No. 519295. It is general information only and does not constitute financial product advice. If any statements made (either alone or together) constitute advice, then the advice is general advice only and does not take into account anyone’s objectives, financial situation or needs. This document is based on information considered to be reliable. It is based on our judgement at the time of issue and is subject to change. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document. Except for liability that cannot be excluded, Infinity Financial Consultants, its directors, employees, agents, and related bodies corporate disclaim all liability in respect of any error or inaccuracy in, or omission from, this document and any person’s reliance on it. This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. If this document contains any performance data, then performance is not a reliable indicator of future performance.